Teaser: Precious metals fell about 3% on Friday after a stronger-than-expected U.S. jobs report reinforced expectations that the Federal Reserve will hold interest

rates higher for longer, citing inflation concerns driven by the Middle East war. Nonfarm payrolls climbed by 172,000 jobs in May, following an upwardly revised 179,000 in April, according to a report from the US Labor Department's Bureau of Labor Statistics. A Reuters poll predicted an increase of 85,000 jobs, following a

previously announced increase of 115,000 in April. Although gold is viewed as an inflation hedge, increasing interest rates have a negative impact on the commodity.

According to CME Group's FedWatch tool, markets are currently pricing in a 72% possibility of a Fed rate hike in December, up from around 50% prior to the jobs

report.

Introduction:

Gold and silver weakened this week as easing crude prices and improving expectations surrounding a potential US–Iran agreement reduced both inflation fears

and safe-haven demand. Markets increasingly focused on diplomatic efforts aimed at extending the ceasefire and restoring normal shipping activity through the Strait of Hormuz, helping unwind some of the geopolitical risk premium that had supported precious metals in recent months. While lower energy prices eased concerns over persistent inflation, they also reduced the urgency for defensive positioning in bullion. Silver also came under pressure as broader commodity sentiment softened. Going into next week, precious metals are likely to remain highly sensitive to developments surrounding US–Iran negotiations, Fed policy expectations, and crude price direction, with further diplomatic progress potentially limiting upside unless broader risk sentiment deteriorates.

WTI crude futures extended their decline this week as growing optimism surrounding a potential US–Iran agreement continued to erode the geopolitical risk premium embedded in energy markets. Expectations that shipping flows through the Strait of Hormuz could gradually normalize encouraged further liquidation of long positions, while traders increasingly shifted focus toward demand-side concerns and the prospect of improved supply availability. The market largely looked through supportive inventory trends as diplomatic developments dominated sentiment. Despite the recent correction, negotiations remain incomplete and uncertainty surrounding regional security continues to linger. Going into next week, crude is expected to remain highly headline-driven, with prices likely to stabilize if diplomatic momentum continues, while any setback in negotiations could quickly revive volatility and support a rebound in risk premiums.

Gold:

Gold traded near $4,300 an ounce on Monday after tumbling nearly 5% last week to its lowest level in more than two months, as renewed tensions in the Middle East drove oil prices higher and fuelled concerns about inflation and interest rates. Iran launched several rounds of missiles toward Israel in a warning against further military actions in Lebanon, though Israel's military said all the projectiles were intercepted and no casualties were reported. The prolonged conflict and the continued nearclosure of the Strait of Hormuz have disrupted energy supplies from the Persian Gulf, supporting higher oil prices and intensifying inflation concerns. At the same time, stronger-than-expected US employment data weighed on bullion last week by reinforcing expectations that the Federal Reserve could raise interest rates later this year. Markets are now pricing in roughly a 70% chance of a Fed rate hike in December, up from around 50% before the jobs report.

Technical View: $4316.03. It is approaching a confluence of the weekly

lower Bollinger Band and the 50-week EMA near $4265–4255, which is a

strong support. However, expanding weekly bands and a sub-zero weekly

MACD suggest this support can break, opening 4098. Resistances at 4370

and 4450 can cap recoveries. A rise above 4615 is needed to attract buyers.

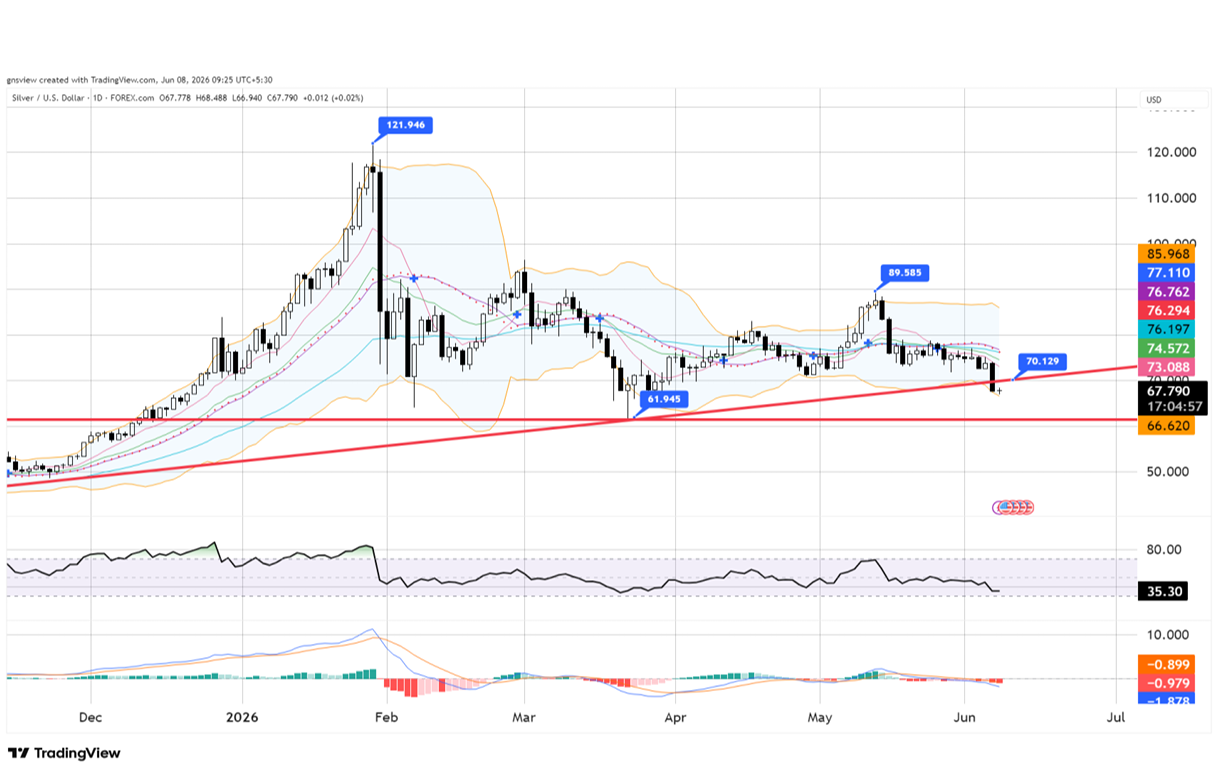

Silver

Silver traded near $68 an ounce on Monday after tumbling nearly 10% last week to

its lowest level in more than two months, as renewed tensions in the Middle East

drove oil prices higher and fuelled concerns about inflation and interest rates. Iran

launched several rounds of missiles toward Israel in a warning against further military

actions in Lebanon, though Israel's military said all the projectiles were intercepted

and no casualties were reported. The prolonged conflict and the continued near

closure of the Strait of Hormuz have disrupted energy supplies from the Persian Gulf,

supporting higher oil prices and intensifying inflation concerns. At the same time,

stronger-than-expected US employment data weighed on precious metals last week

by reinforcing expectations that the Federal Reserve could raise interest rates later

this year. Markets are now pricing in roughly a 70% chance of a Fed rate hike in

December, up from around 50% before the jobs report.

Technical View: $67.79. Resistance seen now at $79/82 to cap for a decline

to $65 or even lower while momentum sustains. Unexpected rise above $86

can negate our bearish outlook.

Crude Oil

WTI crude futures climbed above $92 per barrel on Monday, rebounding after two

consecutive sessions of losses as Iran launched multiple rounds of missiles toward

Israel, warning against further military actions in Lebanon and raising concerns over

the durability of a fragile ceasefire amid stalled peace negotiations. Israel's military

said all incoming missiles were intercepted, with no casualties reported. According to

reports, President Donald Trump criticized Israel's strikes on Beirut and said he would

urge Prime Minister Benjamin Netanyahu to avoid retaliatory action against Iran,

while also calling on Tehran to resume negotiations. Meanwhile, the protracted

conflict and the ongoing near-closure of the Strait of Hormuz have cut off energy

supplies from the Persian Gulf, keeping oil prices elevated. Separately, OPEC+

approved another increase in July oil production quotas of 188,000 barrels per day

despite persistent supply risks linked to tensions in the Middle East.

Technical View: $93.52. Weekly chart is tilted to the downside for a test of

the 20-week EMA near 83.50 or even the weekly super trend support at

78.20. Resistances are at 92.35 and 93.65, which can cap upticks. A rise

above 94.50 can make the outlook uncertain. A break above 98.30 is needed

to turn bullish and open 104.00.

Copper

U.S. tariff uncertainty continues to distort and tighten the global copper market,

according to market watchers. Washington is expected to decide whether to extend

import tariffs to refined copper, a move that could have significant implications for

global supply flows. Last year, expectations of tariffs drove LME copper prices higher

as U.S. buyers accelerated purchases and built inventories ahead of potential trade

restrictions, reducing available supply elsewhere. "The upcoming U.S. Commerce

Department report, due by the end of June, represents a potentially important

catalyst," analysts at Saxo Bank say. "A recommendation supporting future tariffs

could encourage further inventory accumulation ahead of implementation, while a

decision not to proceed could trigger an unwinding of the current premium and some

temporary pressure on prices."

Technical View: $6.28. Supports to be observed at $6.15/6.10 where dips can hold for a rise to $6.65/6.70 near term. Only an unexpected breakdown below $6.10 could dampen our bullish expectations.